Rethinking Synergy in Mergers & Acquisitions

We need to expand our conceptualization of where value comes from in M&A. In a recent study, Emilie Feldman and I developed the five synergy framework to do just that.

Mergers and acquisitions (M&A) are common, costly, and consequential. Every year thousands of transactions, costing acquirers billions, reshape entire industries in long-lasting ways. Entire consulting and investment practices are designed to help firms make better decisions about these acquisitions and profit from the market’s reaction to them. The central question for all actors involved is: How do M&A create value? Synergy has long been the buzzword used to answer that question. Managers trying to justify deals tout the immediate and long-term synergies a deal is expected to produce. Analysts trying to price deals scrutinize the validity of synergy claims. And students in MBA classes are taught to look for “1+1=3” gains from business combinations.

But what if I told you that we have been systematically thinking about only 40% of the kinds of synergies generated by M&A? This is exactly the point that my brilliant colleague, Emilie Feldman, and I make in a paper that was recently accepted for publication in the Academy of Management Review -- one of the top academic management journals.

We conducted a thorough analysis of previous research on M&A, and built on our combined decades of researching and teaching corporate strategy, to assess the state of our understanding of the concept of synergy. We realized that both academics and practitioners involved in M&A have predominantly considered only two (2) explanations of synergy, overlooking three (3) additional sources of economic value creation made possible by these transactions.

Based on that realization, we make three crucial points:

Point #1: There are five distinct potential sources of synergy when two firms combine.

I’ll provide a brief definition and offer an example of each using the case of mergers in the U.S. airline industry.

Internal synergies arise from the combination of assets or capabilities that the two firms own and control fully (not shared with a third party).

Example: Airline combinations increased the utilization of airplanes by consolidating passengers in overlapping routes, and reduced costs by sharing personnel, IT systems, and marketing budgets.

Market power synergies arise when the combination gives the firm increased leverage in competitive interactions, such as weakening a pre-existing rival, increasing pricing influence over buyers, or lower the influence of suppliers.

Example: By consolidating with pre-existing competitors, airlines were able to charge higher prices along many routes.

Relational synergies arise when the combined assets of the two firms enhance the value of other assets shared with a third party that has a contractual relationship with one or both of the combining firms. The third party could be any other firm like an alliance partner, a distributor, or a supplier. Notice that this requires joint value creation (win-win) by the combined entity and a third party, rather than zero-sum (win-lose) value creation as in the case of market power.

Example: When American Airlines and U.S. Airways merged, they were able to jointly create more profit with their credit card partners (City and Barclays). The airlines could offer more clients to the card companies, and the companies could offer better terms and rewards to clients. Both sides gained more profit.

Network synergies arise when the combination of the two firms’ external networks of business relationships restructure the network in a way that puts the combined entity in a better structural position (e.g. the merged firm becomes more central in the industry alliance network). The gain here comes from the combined total business partnerships of both firms, rather than from improving any individual partnership as in relational synergies.

Example: Combined airlines could increase their centrality in one of the major constellation alliances (e.g. OneWorld, SkyTeam). Further, they could occupy a more central position in the network of service providers surrounding an airline business (hotels, car rentals, etc.), allowing them to access more resources from the network and better coordinate the flow of services.

Non-market stakeholder synergies arise when the deal allows the combined firm to improve its relationships or reputation with external stakeholders such as regulators, communities, NGOs, etc.

Example: Airlines depend on the goodwill of many non-market stakeholders, such as labor unions, communities surrounding major hubs, and transportation regulators. The mergers often allowed them to develop better relationships with these stakeholders by offering more value to them. For example, the Delta-Northwest deal allowed Delta to bring more jobs to the Salt Lake City area and improve goodwill with that community and its regulators.

The overwhelming focus of M&A practice and research is on the first two synergy types (internal and market power), because of an undue emphasis on synergies from assets that are owned by the combining firms and governed through competitive interactions with rivals. This has led to overlooking the latter three (relational, network, stakeholder), which are based on assets that are shared among many firms and governed through cooperative interactions.

Not all deals will involve every single one of the five synergies. But most deals have the potential to create economic value through more than just one source of synergy. Overlooking the full landscape of potential gains from M&A creates the risk of missing out on significant unimagined gains. This problem is exacerbated when one considers our next point.

Point #2: The total value created by an acquisition is the sum of each individual synergy gain and the interactions (positive or negative) across synergy types.

Each of the five synergy types creates value through a distinct mechanism, as just summarized. But it’s possible that they interact with one another positively or negatively. We label the positive interactions as “co-synergies” and the negative interactions as “dis-synergies” in the paper.

For example, when Johnson & Johnson acquired the robotic surgery company Auris in 2019, it gained improved capabilities in lung-cancer diagnosis and treatment. But the deal also had knock on effects by enhancing the value of J&J’s alliance with Alphabet -- a pre-existing alliance focused on developing robotic surgery technology. This represents a co-synergy between the typical internal gains reported in the business press and the less visible relational synergy from making the partnership with Alphabet more valuable. An example of a dis-synergy occurred when CVS and Aetna merged. The rationale for the deal was based on internal complementarities between the pharmacy and insurance businesses (internal synergy) and, less touted publicly, more control over the price of drugs (market power synergy). But this resulted in a negative outcome in terms of relationships with stakeholders who opposed the deal, such as the AIDS Healthcare Foundation publicly expressing worries that the combination would result in suboptimal care and confidentiality breaches for AIDS patients. Worsened stakeholder relationships can severely harm companies post-acquisition, eroding the value they thought they were gaining by combining.

Of course, these are only two of many possible examples. Each deal will create its unique set of co- and dis-synergies. But the implications of this are profound, because it suggests that the total value created by a deal is as follows:

Realized Value = ∑i * Synergyi + ∑i,j * Co-Synergyi,j – ∑i,j * Dis-Synergyi,j – Price Premium

The first term refers to the summation of each individual synergy on a standalone basis. The second term captures the reinforcing gains that arise why any pair of synergy sources interact positively. And the third term captures the losses that arise why any pair of synergy sources interact negatively. This is a much more comprehensive notion of total value created by an M&A deal than previously thought. It suggests that managers, consultants, analysts, and students need to develop new methods of measuring and valuing synergy sources. It also suggests that managers may have more avenues to both create and destroy value than previously thought. And it means that the execution of a successful deal is more complex than typically thought. We hope this study can create something of a revolution in the practice and teaching of M&A strategy, finance, and implementation.

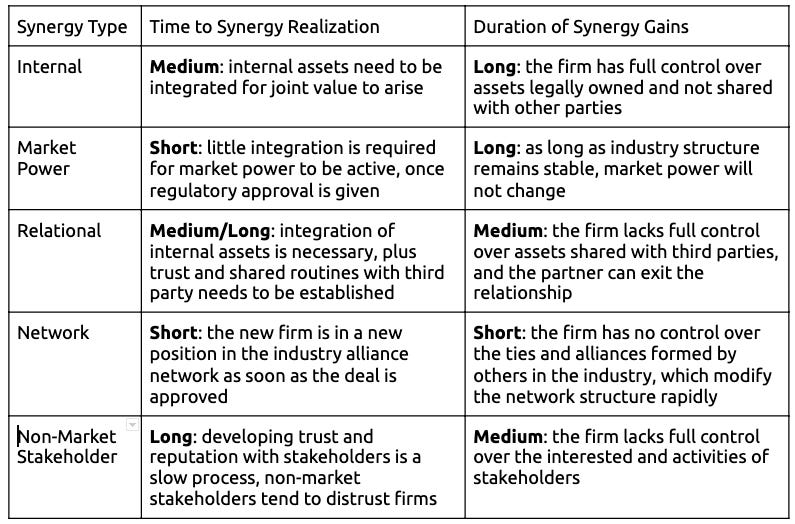

Point #3: Each synergy type has a unique lifecycle, involving different timing of initial realization and a different duration of gains.

Understanding that there are five distinct potential sources of synergy is also critical in the post-acquisition phase, because achieving a synergy is distinct from expecting one. Our core insight here is that each synergy needs to be managed differently because it has a unique lifecycle. By lifecycle, we refer to the timing of two critical phases: the initial realization of the synergy (how long will it take to see the gains?) and the length of time the underlying assets will produce synergistic gains before fading away (how long will the synergies last?).

Our framework suggests that two factors determine the duration of each phase: the amount of post-merger integration required influences the speed of initial realization, while the control the firm has over the underlying assets influences the duration of synergy gains. These two factors lead to distinct lifecycles across the five synergies, as follows:

The full details of our logic are in the paper, and are hard to fully convey in a brief summary. But the managerial implications are profound: Obtaining the full benefits of an acquisition requires managing the process differently depending on the type of value the firm seeks. Some benefits will arise quickly and others not, and some will erode fast and others slowly. The figure below offers an illustration of how the timing of gains may differ across synergy types. This framework can thus help provide a more complete map to managers involved in the post-deal phase, as well as to analysts involved in evaluating the outcomes of business combinations.

We believe this expanded conceptualization of synergy in M&A can help everyone involved in executing or analyzing these important deals by offering a more comprehensive notion of where value comes from pre-acquisition and how it is achieved post-acquisition.

Emilie and I are excited to share this new framework. We also realize it’s new to the practice and study of M&A, and are looking for examples of the different concepts involved and for better ways to convey those concepts. We would love for you to share any examples or ideas to help us! Please do so by adding a comment below. We’ll be thankful for your contribution.